For any South African business trading internationally, managing payments can feel a lot like trying to navigate a ship through choppy, unpredictable seas. This guide is your map. We're here to explain why a smart strategy to exchange currency in South Africa is non-negotiable for importers and exporters alike, and give you the real-world insights you need to protect your profits.

Why a Smart Currency Strategy Is No Longer Optional

If you're buying or selling across borders, every single transaction involves foreign exchange (FX). It's that simple. Whether you're an importer paying a supplier in US Dollars or an exporter getting paid in Euros, your company’s financial health is directly linked to how well you handle that currency conversion.

Get it wrong, and you can watch your profit margins disappear in an instant. Get it right, and you gain a serious competitive edge. The real challenge is the volatile nature of the FX market. The Rand's value can swing wildly based on anything from local economic news to global market jitters, meaning the old way of doing things just doesn't cut it anymore.

The Key Players in Currency Exchange

To get a handle on the FX landscape, you first need to know who the main providers are. Each option comes with its own mix of costs, speed, and service, so the "right" choice really depends on what your business needs.

- Traditional Banks: They're the default for many businesses, offering a sense of security and a broad suite of services. The trade-off? Banks are notorious for wider exchange rate spreads (the margin they add on top) and fee structures that can be difficult to unpack.

- Bureaux de Change: You'll see these in airports and city centres. They’re built for tourists, not businesses, and their rates simply aren't competitive for commercial-sized transactions.

- Fintech Specialists: This is where modern providers like Zaro come in. These companies focus specifically on international payments, which means they can often offer much tighter, real-time exchange rates, lower fees, and a far smoother digital platform.

Common Challenges Businesses Face

Just picking a provider is only half the battle. A few common obstacles can trip up even experienced businesses when exchanging currency. Knowing what they are is the first step to avoiding them.

The core issue for most businesses isn't just the exchange rate itself, but the lack of transparency around the total cost. Hidden fees and unpredictable markups can turn a profitable deal into a loss without warning.

Everyday hurdles include those volatile exchange rates that make forecasting a nightmare, confusing regulatory hoops to jump through with the South African Reserve Bank (SARB), and all the hidden costs baked into transactions. We’ve designed this guide to give you the clarity and tools to master these elements, making sure every international payment you make is both compliant and cost-effective.

Here’s the rewritten section, designed to sound more natural and human-written, as if from an experienced expert.

How Foreign Exchange Actually Works

At its core, the foreign exchange (or FX) market is simply a massive, global marketplace where currencies are bought and sold. It’s not some abstract concept; think of it as a giant, non-stop auction where the value of one currency is constantly being measured against another. For your business, this isn't just theory—it’s the engine that determines the real cost of every single international payment you make.

Every time you exchange currency in South Africa, whether you're paying a supplier in China or getting paid by a client in Europe, you're stepping into this market. The price you pay is the exchange rate, which is just the cost of buying one currency using another.

But here’s the tricky part: that rate is never static. It moves every single second, nudged by a relentless flow of economic news, political shifts, and general market mood. Getting a handle on these forces is the first step to making smarter financial decisions for your business.

What Makes Exchange Rates Fluctuate

The value of the South African Rand (ZAR) is really a reflection of the country's economic health and its relationship with the rest of the world. A few key factors are always in play, creating the volatility we see every day.

Here are the main drivers to watch:

- Interest Rates: When the South African Reserve Bank (SARB) hikes interest rates, it can attract foreign investors looking for better returns on their cash. This increased demand for the Rand makes it stronger. The opposite happens when rates are cut.

- Inflation: Simply put, high inflation eats away at a currency's buying power, weakening it over time. A country with consistently low inflation usually sees its currency value climb.

- Political and Economic Stability: A stable government and a growing economy build confidence. When investors feel confident, they buy into the country and its currency. Any hint of uncertainty, however, often sends the Rand tumbling.

- Commodity Prices: South Africa is a major exporter of resources like gold, platinum, and coal. Because of this, the Rand's value is often tied to the global prices of these commodities. A surge in the gold price, for instance, almost always gives the ZAR a boost.

We saw this in action throughout 2025, when the Rand showed significant strengthening against the US Dollar. As of December 2, 2025, the USD/ZAR rate was 17.0919, a major recovery from its all-time high of 19.93 back in April 2025. That comeback represents a 5.50% appreciation of the Rand over 12 months, proving just how much these factors can shift its value. You can dive deeper into historical ZAR performance trends to see these forces at play.

Mid-Market Rate vs. Customer Rate: The Hidden Cost

This is one of the most important concepts for any business to get right. There's a big difference between the exchange rate you see on Google or the news and the rate you actually get.

The "mid-market rate" is the true exchange rate. It's the midpoint between what buyers are willing to pay and what sellers are asking for on the global markets. Think of it as the wholesale price—it's what banks use to trade huge sums with each other.

But that’s almost never the rate your business is offered. Instead, you get the customer rate, which includes a markup that your provider adds on top. This markup is called the spread, and it’s how most banks and traditional brokers make their money. It's the retail price, and just like in a shop, you always pay more than the wholesale cost. This is the model that fintech specialists like Zaro are changing, by giving businesses access to the mid-market rate and getting rid of the spread.

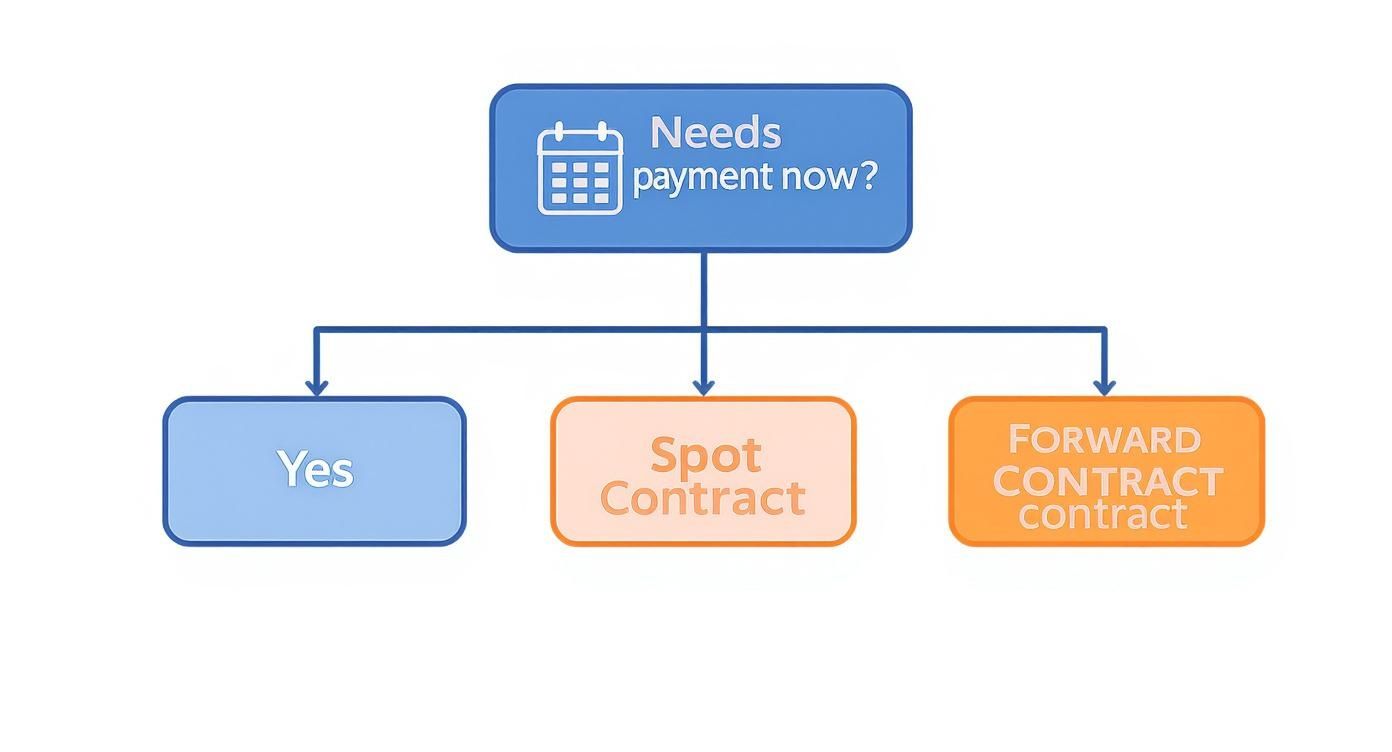

Spot Contracts vs. Forward Contracts

When you exchange currency, you’ll typically use one of two types of agreements, depending on what you need to do. Knowing the difference is crucial for managing your cash flow and protecting your business from risk.

1. Spot Contracts

This is your standard, everyday transaction. A spot contract is for an immediate currency exchange, settled "on the spot" or within a couple of business days. It’s perfect for paying an invoice that's due right now. You agree on today's rate, and the transfer happens straight away. Simple.

2. Forward Contracts

A forward contract, on the other hand, is a powerful tool for planning ahead. It lets you lock in an exchange rate today for a payment that will happen in the future. For example, if you know you have to pay a $100,000 invoice in three months, you can secure the rate now. This completely removes the risk that the Rand might weaken against the Dollar before the payment is due, giving your business total cost certainty and protecting your profit margin from nasty surprises.

Choosing Your Currency Exchange Provider

Picking the right partner to exchange currency in South Africa is one of the most critical financial decisions your business will make. It’s not just about chasing the best rate on a given day. It’s about finding a provider that fits how you operate—one that delivers on speed, transparency, and sheer reliability when you need it most.

The market is really broken down into three types of providers, and the differences between them can be stark. A few points on an exchange rate or a "small" hidden fee might not sound like much, but on a large international invoice, it can easily add up to thousands of Rands vanishing from your profit margin.

Let's unpack your options.

Traditional Banks

For most businesses, the default choice is their main bank. It feels safe, familiar, and convenient to keep everything under one roof. Banks are, of course, well-regulated and have the muscle to handle large, complex transactions without breaking a sweat.

But that convenience almost always comes with a hefty price tag. Banks are notorious for adding a significant spread (a mark-up) to the real exchange rate. This is a major profit centre for them. On top of that, their fee structures can be a maze of transfer fees, intermediary bank charges, and other admin costs that only become clear after the fact. The whole process can also be surprisingly slow, sometimes taking several business days for funds to land.

Bureaux de Change

You’ve seen these kiosks at airports and shopping centres. They serve a purpose for tourists needing a bit of cash for their holiday, but for a business, they are a non-starter.

Their entire business model is based on high-volume, low-value cash exchanges. This means they use extremely wide spreads and often charge high commission fees to make a profit. For a commercial payment of any real size, their rates are simply uncompetitive. Using them to pay an international supplier would be an incredibly expensive mistake.

Modern Fintech Payment Specialists

A newer breed of provider has come along to challenge the old way of doing things. Fintech specialists, like Zaro, are laser-focused on one thing: international payments. This specialisation means they can operate far more efficiently and pass those savings directly on to you.

These platforms typically offer much tighter exchange rate spreads—in some cases, no spread at all, giving you direct access to the mid-market rate you see on the news. They’re built on slick digital platforms designed for speed and clarity.

The big shift with a fintech specialist is their entire philosophy. They're not trying to make a huge profit on your exchange rate. Instead, they provide a streamlined, low-cost service, which means your business keeps more of its hard-earned money with every single transfer.

If your business values efficiency, low costs, and knowing exactly where your money is at all times, these specialists are a game-changer. They also tend to build powerful tools like forward contracts right into their platforms, making it much easier to protect your business from a volatile Rand.

This simple chart helps clarify which contract type to use, depending on when your payment is due.

As the decision tree shows, if you need to pay right away, a spot contract is your go-to. If you need to lock in a rate for a future payment, a forward contract is the smart move.

Comparing Currency Exchange Channels for Businesses

To really see the difference, it helps to put these providers side-by-side and compare them on the factors that actually matter to your bottom line.

| Feature | Traditional Banks | Bureaux de Change | Fintech Specialists (e.g., Zaro) |

|---|---|---|---|

| Exchange Rate Spread | Wide; a significant source of their profit. | Extremely wide; designed for tourists, not businesses. | Very tight or zero; often provide the mid-market rate. |

| Fees | Often includes transfer fees, SWIFT fees, and receiving fees. | High commission fees are common. | Low, transparent, or a flat fee model. Often no SWIFT fees. |

| Transaction Speed | Slower; typically takes 2-5 business days. | Instant for cash, but not suitable for business payments. | Faster; often completed within the same day or 1-2 days. |

| Transparency | Can be low; total costs are not always clear upfront. | Rates are displayed, but overall cost is high. | High; clear breakdown of rates and any applicable fees. |

| Risk Management Tools | Available, but may require a dedicated relationship manager. | None available. | Integrated into the platform (e.g., forward contracts). |

| Best For | Businesses prioritising a long-standing bank relationship over cost. | Tourists and individuals needing small amounts of cash. | Businesses focused on cost-efficiency, speed, and transparency. |

Ultimately, there’s no single "best" provider for everyone—it hinges on what your business needs. If you make frequent international payments and want to cut costs while boosting efficiency, a fintech specialist is almost certainly the right call. If you value keeping all your finances in one place and aren't as sensitive to the costs, sticking with your bank might work for you.

The key takeaway is to look past the advertised rate and dig into the total cost and service you’re actually getting.

Uncovering the True Cost of Exchanging Currency

That exchange rate you see splashed across the news or on a currency converter? Think of it as a starting point, not the final price. When your business needs to exchange currency in South Africa, the real cost is often buried in a string of fees and markups that quietly eat into your profits. Getting wise to these hidden costs is the first and most critical step to protecting your bottom line.

Many business owners fall into the trap of hunting for the "best rate." But focusing only on the rate is like judging a car by its paint job while ignoring what’s under the hood. The total cost of any international payment is much more than that one number. Providers, especially the big traditional banks, have perfected the art of building their profit into complex fee structures that you often don't see until the money has already left your account.

These costs aren't always laid out clearly, which makes comparing providers a real headache. To make a smart decision, you have to look at the entire picture, not just the attractive rate they dangle in front of you.

Beyond the Exchange Rate Spread

The spread—that's the markup a provider adds to the real, mid-market exchange rate—is a big part of the cost, but it's far from the only one. A single international payment can get hit with several other fees, each one taking a slice of the pie before it reaches your supplier.

Here are the usual suspects you need to watch for:

- Transfer Fees: This is the most straightforward charge—a flat fee just for initiating the payment. It can be anything from a few hundred Rand to over a thousand, and you pay it regardless of how much you're sending.

- SWIFT Fees: When money moves through the global SWIFT network, it often hops between several intermediary or correspondent banks. Each bank in that chain can take a cut, and these fees are notoriously difficult to predict.

- Receiving Fees: Just when you think you’re done, the beneficiary's bank might charge its own fee for simply receiving the funds from overseas. This amount gets deducted before the money lands, meaning your supplier gets less than you actually sent.

The best exchange rate doesn't automatically mean the cheapest deal. A provider with a slightly less attractive rate but zero transfer or SWIFT fees could easily save your business thousands in the long run.

A Real-World Cost Comparison

Let's put some numbers to this. Say your South African business has a $50,000 invoice to pay a supplier in the US. The true mid-market rate on the day is R18.00 to the Dollar.

Here’s a typical breakdown of how the costs might look with two different types of providers:

Provider A: A Traditional Bank

- Offered Rate: R18.36 (a 2% spread)

- Total Rand Cost: R918,000

- Transfer Fee: R500

- SWIFT/Receiving Fees: R800 (a reasonable estimate)

- Total Cost to Your Business: R919,300

Provider B: A Fintech Specialist (like Zaro)

- Offered Rate: R18.00 (the real mid-market rate)

- Total Rand Cost: R900,000

- Transfer Fee: R0

- SWIFT/Receiving Fees: R0

- Total Cost to Your Business: R900,000

On this one payment, the business saved R19,300 by choosing the fintech specialist. If you make dozens of these payments a year, you’re suddenly talking about a massive financial impact. This is why you should always calculate the Total Cost of Transaction (TCT), not just glance at the headline rate.

To get a deeper understanding of how rate fluctuations can affect your overall costs, it's a good idea to look into performing sensitivity analysis. This exercise can help you model different scenarios and build more resilience into your financial planning.

The simple takeaway? Always ask for a full breakdown of all potential charges upfront. It's the only way to dodge nasty surprises and make sure you’re getting the most for your money.

Navigating South Africa's Regulatory Landscape

When your business needs to exchange currency in South Africa, compliance isn't just a box-ticking exercise—it's absolutely non-negotiable. Every single cross-border payment is scrutinised by the South African Reserve Bank (SARB) to maintain financial stability and stamp out illicit fund flows.

The rules can feel a bit daunting at first, but with the right partner and a clear process, they are entirely manageable. Think of SARB's exchange control regulations as the guardrails keeping our country's financial system safe. For your business, this means every international payment needs a clear reason, the right paperwork, and correct reporting. Getting this wrong can lead to frustrating delays, hefty penalties, or worse.

This is where your Authorised Dealer comes in. An Authorised Dealer is simply a financial institution—like a traditional bank or a licensed fintech provider—that has SARB's official permission to handle foreign exchange. They are the gatekeepers, ensuring every rand you send or receive complies with the law.

What is Balance of Payments Reporting?

One of the most important parts of this process is Balance of Payments (BoP) reporting. This is a mandatory declaration you make for every international transaction, explaining precisely why the money is moving. It’s not just red tape; it's how SARB tracks the flow of capital for crucial economic analysis.

For example, when you’re paying an overseas supplier, you need to understand the Bopcard Reporting Requirements. Each payment must be assigned a specific category code that describes its purpose, whether it's for imported goods, professional services, or a software licence.

It's your Authorised Dealer's job to submit this BoP report to SARB for you. But remember, providing them with accurate and timely information is your legal responsibility.

Getting Your Compliance Ducks in a Row

The regulatory side of things becomes much easier when you know what's required. While a good payment provider will guide you, it’s vital to have your own documentation in order.

Your Essential Document Checklist:

- The Commercial Invoice: This is the bedrock of any trade transaction. It proves a legitimate deal took place and must clearly show the goods or services, who the buyer and seller are, and the total amount owed.

- Proof of Import/Export: For physical goods, this is often the customs documentation (like a SAD 500 form) showing the items have officially crossed the border.

- Tax Clearance Certificate (TCC): For certain payments, especially larger amounts, SARS will require a TCC to confirm your tax affairs are up to date before the funds can leave the country.

Don't Forget About Repatriation

Compliance isn't just about sending money out; it applies when you're getting paid, too. If your business exports goods or provides services to international clients, you are legally required to bring those foreign currency earnings back into South Africa.

This process is called repatriation, and it must typically happen within 180 days of you earning the money. This rule ensures that export earnings flow back to support the local economy and strengthen the country's foreign currency reserves.

Working with a modern provider like Zaro can take the pain out of this by helping to automate the documentation and reporting for repatriated funds. When the complexities of BoP codes and regulatory submissions are handled for you, compliance stops being a burden and simply becomes a smooth, background process.

Making Your First International Payment Step by Step

Sending money across borders for the first time can feel a bit daunting. There are new terms, compliance checks, and a general sense of "am I doing this right?". Don't worry. When you break it down, the process is actually quite logical.

This guide walks you through the entire journey, from setting up your account to the moment your funds land safely with your recipient. Think of it as a repeatable checklist for every time you need to exchange currency in South Africa, giving you the confidence to manage your global payments smoothly.

Step 1: Onboarding and Verification

Before any money can move, you need to be properly set up and verified with your chosen provider, whether that's a bank or a fintech partner like Zaro. This isn't just red tape; it's a mandatory compliance process called Know Your Business (KYB). It’s a legal requirement designed to prevent financial crime, and every legitimate provider has to do it.

To get verified, you’ll usually need to have these documents handy:

- Your company registration papers (like your CIPC documents).

- Proof of your business address.

- ID documents for the company's directors and major shareholders.

Pro-Tip: Get all your KYB documents scanned and ready in a folder before you start. What can often drag on for days can be wrapped up in a few hours if you’re organised, meaning you can get down to business much faster.

Step 2: Getting a Live Quote and Booking Your Deal

Okay, your account is live. Now for the important part: seeing what your payment will actually cost. The next step is to request a live exchange rate quote for the currencies you need to trade, for example, ZAR into USD. A good platform will show you the real-time rate and lay out any fees clearly, so there are no surprises.

If the numbers look good, you then book the deal. This is a crucial action. It locks in that specific exchange rate for a set amount of time. Why does that matter? It shields your business from the risk of the market suddenly moving against you while you’re busy organising the funds. It gives you total certainty over your costs.

Step 3: Funding the Transaction and Adding Beneficiary Details

With your rate secured, it's time to fund the deal. This is usually as simple as making a local EFT in Rands from your business bank account to the details your payment provider gives you.

At the same time, you'll provide the details for the person or company you're paying. Attention to detail here is everything—getting it wrong can lead to failed payments, frustrating delays, and even extra fees.

Make sure you have the following information, and check it twice:

- Beneficiary Name: Their full, official name.

- Beneficiary Address: Their complete physical address.

- Bank Name and Address: The details of the bank they use.

- Account Number/IBAN: The specific account identifier.

- SWIFT/BIC Code: The bank’s unique global code.

A simple typo in an account number or SWIFT code is the number one reason payments get stuck or rejected. Once your provider receives your funds and you’ve confirmed the beneficiary details, they’ll handle the currency conversion and send the payment on its way.

Got Questions About Currency Exchange? We’ve Got Answers.

When you're running a business in South Africa, stepping into the world of foreign exchange can feel a bit daunting. Lots of questions come up. We hear them all the time, so we’ve put together straightforward answers to the most common ones.

How Long Does an International Payment Take?

The honest answer? It really depends on who you use. If you go the traditional route with a bank, you’re often looking at a wait of 3-5 business days. Your money has to jump through a few hoops in the old-school SWIFT network.

But it doesn't have to be that slow. Newer fintech providers have found smarter, more direct ways to send money across borders. With these services, your funds can land in your recipient's account within 24-48 hours, and sometimes even on the same day. That kind of speed can make a huge difference in keeping your suppliers happy.

What is the Best Time to Exchange Currency?

Trying to "time the market" is a bit of a lottery, even for the pros who do this all day. For a business, guessing games are a risky strategy. The better move is to focus on what you can control: certainty.

Rather than trying to predict the future, lock in a good exchange rate when you see one. If you know you have a big payment coming up, a forward contract lets you fix the rate today. It takes the guesswork out of the equation and protects your bottom line from any sudden market swings.

Can I Hold Foreign Currency in a South African Account?

Absolutely. South African businesses are permitted to open a Foreign Currency Account (FCA) with an authorised dealer. This lets you keep funds in major currencies like US Dollars, Euros, or British Pounds without having to convert them back to Rand straight away.

An FCA is a game-changer if you regularly get paid and also have to pay suppliers in the same foreign currency. It means you can manage your cash flow much more effectively and sidestep the conversion fees you'd otherwise pay on every single transaction.

Ready to stop overpaying on international transfers and simplify how you exchange currency in South Africa? Zaro offers real exchange rates with zero spread and no hidden SWIFT fees, giving you full transparency and control over your global payments. Discover a smarter way to manage your FX with Zaro.