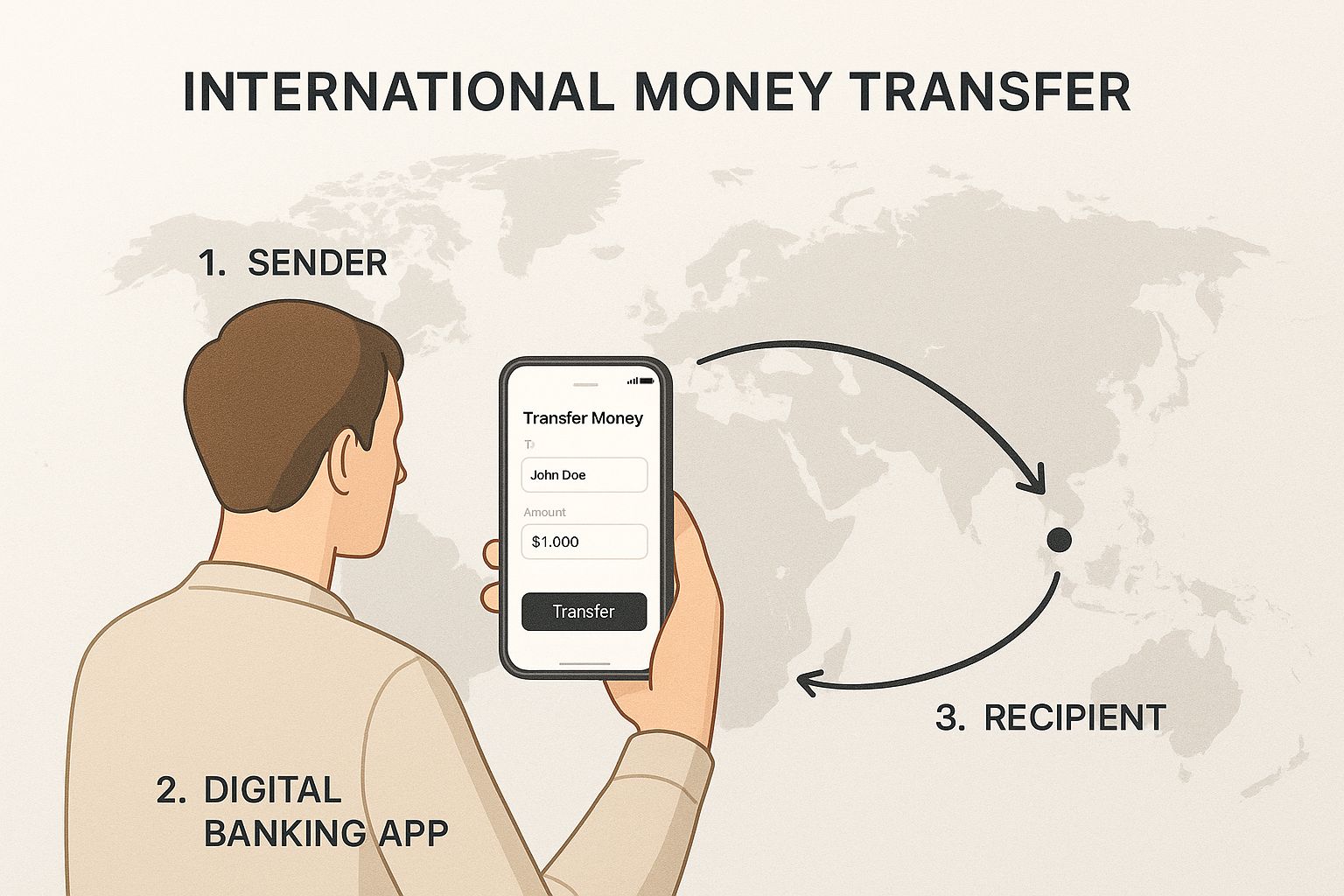

At its core, an international monetary transfer is just what it sounds like: sending money from one country to another. For a business in South Africa, this could mean paying a supplier in Germany for new machinery or getting paid by a client based in the United States. It's a fundamental part of doing business in a connected world.

A South African Business Guide to Global Payments

In today's global market, getting international payments right isn't just an admin task—it's a crucial part of your business strategy. Think of it like a global relay race. Your money is the baton, and it needs to be passed smoothly between different banks, systems, and countries to get to the finish line without being dropped or held up.

For any South African company with global ambitions, these transfers are the lifeblood of international trade. They're how you:

- Pay overseas suppliers: Get the raw materials or finished products you need to operate.

- Receive client payments: Bring in revenue from customers no matter where they are.

- Manage international payroll: Pay your remote team members or contractors abroad.

But let's be honest, the process is often anything but simple. The old ways of sending money across borders can be painfully slow, surprisingly expensive, and frustratingly opaque.

The Challenge with Traditional Transfers

Trying to manage cross-border payments often feels like you're navigating a maze blindfolded. Hidden fees pop up out of nowhere, eating into your profits, while unexpected delays can damage relationships with key suppliers. A payment that shows up two days late might not sound like a disaster, but it can throw your entire supply chain into chaos.

The biggest headache for most businesses is the sheer lack of transparency. When you can’t see the real exchange rate you're getting or figure out what every intermediary bank is charging along the way, you lose control. It becomes impossible to accurately forecast your cash flow.

Getting to grips with how an international monetary transfer actually works is the first step to solving these problems. Once you know how to spot hidden costs and handle the compliance side of things, you can turn a major frustration into a real competitive edge. This guide will walk you through it, ensuring your money gets where it needs to be, on time and in full.

How Cross-Border Payments Actually Work

Have you ever stopped to think about what really happens after you click ‘send’ on an international payment? It's easy to assume the money zips straight from your account to the recipient's, but the reality is far more complicated. Think of it less like a direct flight and more like a long-haul journey with a few, often invisible, layovers.

To get why traditional cross-border payments can be so slow and expensive, you have to understand the system that’s been running the show for decades: the correspondent banking network. It’s essentially a global web of banks that hold accounts with each other to move money across borders.

If your South African bank doesn't have a branch in, say, Germany, it can't just send the money there directly. Instead, it relies on these "correspondent" or "intermediary" banks to pass the payment along. Each stop on this journey adds time—sometimes days—and, you guessed it, a fee for their trouble. This is the main reason why an international monetary transfer often lands with a chunk missing from the original amount.

The Role of SWIFT

Orchestrating this complex relay race is a system called the Society for Worldwide Interbank Financial Telecommunication, better known as SWIFT. Here's a common misconception: SWIFT doesn't actually move any money. It’s a highly secure messaging network that sends payment instructions—the who, what, where, and how much—from one bank to another.

Think of SWIFT as the air traffic control for global finance. It tells your bank, all the intermediary banks, and the final recipient's bank precisely where the funds need to go. It’s a robust and trusted system, but it’s still just the messaging layer on top of that old, clunky network of correspondent bank "layovers."

This is the typical path your money takes.

As you can see, those extra steps are where the delays and hidden costs creep in, long before your funds reach their destination.

A Modern Alternative to the Old System

This is where the new wave of fintech platforms comes in. They were built to bypass this convoluted network entirely. Instead of routing your payment through a chain of banks, they often use their own network of local bank accounts in different countries to create a much more direct route.

The process is refreshingly simple:

- You pay into the provider’s local South African account in Rands.

- The platform then pays out from its local account in the destination country.

- The money never technically crosses a border through the old correspondent system.

This model is a game-changer. By cutting out the costly middlemen, it enables much faster settlement times and significantly lower fees. This kind of efficiency is no longer a "nice-to-have" for businesses. For many companies, a vital first step into international markets involves navigating processes like opening a business bank account in Dubai or other global trade hubs, which makes having a reliable payment partner even more critical.

This move toward better payment rails isn't just a commercial trend; it's a strategic priority right here at home. The South African Reserve Bank (SARB) is actively working to modernise the system for everyone.

The government’s Vision 2025 framework is focused on making different payment systems work together seamlessly. A key goal is to drive down costs in crucial remittance corridors within the Southern African Development Community (SADC), which see around R6.2 billion in transfers every year. This broader context helps explain why a modern international monetary transfer solution isn’t just about convenience—it’s essential for our economic future.

What You're Really Paying for International Transfers (And Why They Take So Long)

When you see an advertised fee for an international transfer, take it with a grain of salt. That number is usually just the tip of the iceberg. What you see upfront is rarely what you end up paying, thanks to a web of hidden charges and frustrating delays that can blow up your budget and mess with your timeline.

To get a real grip on your cash flow, you have to dig deeper than the initial quote. The true costs are often buried in confusing fee structures and poor currency conversion rates, slowly eating away at your profits with every single payment you make.

Unpacking the Hidden Costs

The biggest culprit is almost always the exchange rate markup. You might also hear this called the 'spread'. Let's be clear: banks and most traditional services almost never give you the real, mid-market exchange rate – the one you find on Google or Reuters. Instead, they sneak in a margin for themselves. That margin is their profit, and it comes directly out of your pocket.

That small percentage might not look like much at first glance. But if your business is sending money overseas regularly, or dealing in large amounts, that spread can easily cost you thousands of Rands over a year. It's a sneaky cost that rarely shows up as a line item on your statement, making it almost impossible to track.

Then you have the intermediary bank fees. Think of it like a package being passed from one courier to another. As your money hops through the global banking network, each bank that touches it can skim a "handling fee" off the top. You have zero say in which banks are used or what they decide to charge, which means the final amount that lands in your supplier's account can be a nasty surprise.

While we're talking about transfer costs, don't forget the bigger picture if you're importing or exporting goods. You'll also need to master customs clearance procedures and duties to avoid even more unexpected expenses and hold-ups at the border.

To give you a clearer picture, let's break down how these costs stack up between an old-school bank and a modern fintech platform.

Decoding the True Cost of an International Transfer

| Cost Component | Traditional Bank (SWIFT) | Modern Fintech Platform |

|---|---|---|

| Upfront Transfer Fee | Often a high, fixed fee (e.g., R250-R500 per transfer). | Typically a low, transparent percentage or a small fixed fee. |

| Exchange Rate Markup | High and hidden. Can be 2-5% above the mid-market rate. | Low and transparent. Often less than 0.5% of the mid-market rate. |

| Intermediary Fees | Unpredictable. Multiple banks can charge R150-R750 each. | None. Uses a direct payment network to avoid these charges. |

| Receiving Bank Fees | Yes, the recipient's bank can also charge a fee to process the payment. | None or minimal, as funds are often paid out from a local account. |

As you can see, the advertised fee is just the beginning. The hidden markups and chain of correspondent fees are where the real damage is done.

So, What's Holding Up Your Money?

The speed of an international monetary transfer is just as important as the cost, especially when your suppliers are waiting and your supply chain is on the line. Several things can grind your payment to a halt:

- Clashing Time Zones: It’s simple, but often overlooked. A payment you send from South Africa at 4 PM might not even be seen by a bank in New York until their day begins the next morning.

- Bank Holidays and Weekends: A public holiday in either your country or the receiving country can freeze the entire process, easily adding a day or two to the wait time.

- Compliance Roadblocks: Every single transfer is screened for things like anti-money laundering (AML) and fraud. If a single detail looks slightly off, your payment gets flagged for a manual review, and that can lead to major delays.

These variables make it incredibly difficult to tell your partners when they can actually expect their money. That kind of uncertainty creates friction and can strain even the best business relationships. Understanding these cost drivers and speed bumps is the first step to finding a smarter way to manage your global payments.

Navigating South African Forex Regulations

For any South African business sending or receiving money across borders, compliance isn't just a formality—it’s the bedrock of a smooth operation. The world of foreign exchange (forex) regulations can feel like a maze, but once you understand the key players and their rules, it becomes a lot less intimidating.

The whole system is managed by two main bodies. First, you have the South African Reserve Bank (SARB). Think of them as the architects of the country’s exchange control framework. They set the rules that govern how money flows in and out of South Africa, all with the goal of keeping the economy stable.

Then there’s the Financial Intelligence Centre (FIC), whose job is to clamp down on financial crime. The FIC works to make sure every transaction is above board, preventing issues like money laundering and the financing of terrorism.

Understanding Key Compliance Requirements

To keep both the SARB and the FIC happy, your business has to follow specific verification processes. These are essentially identity and legitimacy checks for everyone involved in a transaction.

Two terms you’ll hear a lot are:

- Know Your Customer (KYC): This is exactly what it sounds like—verifying the identity of your clients, suppliers, or partners to confirm you know who you’re dealing with.

- Anti-Money Laundering (AML): This refers to the broader set of checks and procedures designed to spot and report any suspicious financial activity.

These checks aren’t optional. In fact, failing to provide the right documents or meet KYC and AML standards is one of the top reasons payments get stuck or even rejected, leading to serious business headaches.

The Essential Documentation Trail

To show that your international money transfer is for a legitimate business purpose, you need a solid paper trail. Every single cross-border payment needs to be backed up by the right supporting documents.

Typically, you’ll be asked for:

- A Commercial Invoice: This needs to clearly outline the goods or services you're paying for, linking the money directly to a real business deal.

- BoP Reporting Code: These are mandatory four-digit codes for "Balance of Payments" reporting. They tell the SARB why you're making the payment—for instance, paying for imported goods or professional services. Getting this code right is critical.

- Transport Documents: If you’re paying for physical goods, you'll need proof of shipping, like a bill of lading for sea freight or an airway bill for air cargo.

It might feel like a lot of admin, but these rules serve a vital purpose. They protect the integrity of South Africa's financial system and, just as importantly, shield your business from accidentally getting caught up in illegal activities. When you treat compliance as a core part of your payment strategy, your money moves faster, safer, and without those costly delays.

Untangling the Knots in Cross-Border Payments

For any South African business dealing with international suppliers or clients, making a cross-border payment often feels like a painful, drawn-out process. These aren’t just minor annoyances; they're genuine operational headaches that eat into your profit, damage relationships, and steal time you should be spending on growth.

Think about this all-too-common scenario. You’ve assured a key supplier in Asia that their payment will land by Friday. Friday comes and goes. The money is stuck somewhere in the correspondent banking labyrinth. Suddenly, you're in damage control mode, making apologetic phone calls and trying to keep a crucial relationship intact while your entire production timeline hangs in the balance. That’s the real-world cost of slow, unpredictable transfers.

The Hidden Costs That Erode Your Margins

It’s not just the delays that cause sleepless nights; the financial guesswork is a constant headache. One of the biggest gripes we hear is about the murky, often hidden fee structures of traditional bank transfers. You agree on a price, send the funds, but when the money arrives, unexpected intermediary bank fees have taken a slice out of it. Your supplier is left short, and you’re left looking unprofessional.

This kind of thing chips away at trust and turns a simple transaction into an administrative nightmare. Your finance team ends up bogged down, spending hours trying to reconcile payments and chase down tiny discrepancies when they should be focused on the bigger financial picture.

And then, of course, there’s the constant threat of currency volatility.

A great exchange rate on Monday morning can easily become a loss-making one by Wednesday afternoon. When you're stuck with systems that don't give you real-time rates or the option to lock in a price, you're effectively gambling with your profit margins on every single international deal.

More Than Just a Business Problem

These frustrations point to just how much we rely on getting cross-border payments right. Here in South Africa, these transfers are about more than just business; they play a vital socio-economic role. The World Bank highlights that around 13% of adults in Sub-Saharan Africa depend on international remittances to support their families.

With global remittance flows to countries like South Africa expected to reach $690 billion by 2025, it’s clear that a reliable, efficient system is essential for everyone, from individuals sending money home to large corporations paying suppliers. You can read more about these global remittance trends and their impact.

At the end of the day, sticking with outdated payment methods does more than just cause daily frustration—it actively holds your business back. Each of these common pain points—the unpredictable delays, hidden fees, admin overload, and currency risk—is a roadblock to growth. By identifying them, you can start looking for a modern alternative that finally gives you the speed, clarity, and control you need to thrive in the global market.

Choosing a Modern Fintech Payment Solution

It’s no surprise that after years of dealing with the headaches of traditional banking, South African businesses are looking for a better way. They're finding it in fintech platforms built specifically to fix these old problems.

Instead of relying on the slow and murky correspondent banking system, these modern solutions use direct and efficient payment networks. It’s a fundamental shift in how companies handle their money across borders, moving away from a system of guesswork and delays.

This change puts control squarely back where it belongs: with your finance team.

Regaining Control Over Global Payments

The real magic of a modern fintech platform is that it brings speed and transparency to a process that has historically had neither. By cutting out the multiple intermediary banks, these solutions can settle an international monetary transfer in hours, not days. That’s a game-changer for maintaining strong supplier relationships and keeping operations running smoothly.

This new approach delivers a few key advantages:

- Real Exchange Rates: You see the mid-market exchange rate without any hidden markups. This means you aren’t losing money on the conversion without even realising it.

- Transparent Fees: All costs are laid out upfront. No more surprise deductions from intermediary banks that make reconciling accounts a nightmare.

- Real-Time Tracking: You can watch your payment's progress from start to finish, just like tracking a package. It gives you—and your partners—complete peace of mind.

These features all point to one powerful outcome for your business: financial predictability. When you know exactly how much you’re paying and precisely when the money will land, you can manage your cash flow and forecast with far greater accuracy.

This isn’t just a small local trend; it's part of a massive economic shift across the continent. Remittance flows into Africa are projected to hit $92.2 billion in 2024, an amount that doubles the continent's overseas development aid.

Closer to home, cross-border flows within the SADC region alone are worth around R6.2 billion each year. These figures highlight just how crucial it is to have better payment infrastructure in place. You can dive deeper into the data on the importance of African remittance flows on Remitscope.

By choosing a modern platform, your business can operate more effectively within this vital and growing economic landscape.

Got Questions? We've Got Answers

Making an international payment for your business can feel like navigating a maze. Here are some of the most common questions we hear from South African business owners, along with some straight-talking answers.

What’s the Most Cost-Effective Way to Send Money Abroad?

Your first instinct might be to go through your business bank, but that’s rarely the cheapest route. Fintech platforms have really shaken things up here, offering exchange rates that are much closer to the true mid-market rate and charging fees that are both lower and easier to understand.

Ultimately, the "best" option depends on how much you're sending, where it's going, and the currency involved. It always pays to do a quick comparison before you commit.

What Paperwork Do I Need for an International Transfer?

Getting your documents in order is crucial for staying on the right side of South African regulations. You’ll almost always need to have these on hand:

- A valid commercial invoice that clearly describes the goods or services you're paying for.

- Your company's registration documents to prove your business is legit.

- A completed SARB reporting mandate, making sure you use the correct Balance of Payments (BoP) code for the transaction.

For larger or more unusual payments, you might be asked for extra documentation.

The single best way to avoid delays is to have all your paperwork ready from the start. A clean, complete paper trail is what gets your payment approved and processed smoothly.

How Long Does an International Transfer Actually Take?

This varies a lot. If you go the traditional route with a bank using the SWIFT network, you can expect the money to arrive in 2-5 business days. The delays often happen when the payment bounces between intermediary banks along the way.

On the other hand, modern payment providers can get the job done much faster. Depending on the destination and currency, it’s often possible to complete a transfer within the same day—sometimes even in a matter of minutes.

Ready to experience faster, more transparent cross-border payments? With Zaro, you get real exchange rates with zero spread and no hidden fees, giving you full control over your global finances. Get started with Zaro today.