For South African businesses, the hunt for the lowest spread forex broker usually starts with a painful discovery. That exchange rate you see on Google or the news? That’s not the one you actually get.

Hidden markups, known as forex spreads, are quietly chipping away at your profits with every single international payment you make. This fee is often the invisible barrier between a healthy bottom line and money needlessly lost.

Why Forex Spreads Are a Hidden Tax on Your Business

Think of it like buying produce. Your local supplier buys apples wholesale for R10 a kilogram and sells them to you for R12. That R2 difference is their markup—their profit. The foreign exchange market works in a strikingly similar way.

A forex spread is simply the markup a bank or broker tacks onto the wholesale exchange rate before they offer it to your business.

While it might look like a tiny percentage on one transaction, these costs add up incredibly fast for companies making regular overseas payments. For South African businesses already navigating the Rand's volatility, a wide spread introduces even more financial risk. It can seriously dent your profitability when paying foreign suppliers or bringing international revenue home.

The Real Cost of a "Small" Fee

The tricky part is that this cost is almost always baked into the exchange rate itself, which makes it hard to see. It’s not a separate line item on your statement like a standard transfer fee.

Instead, it's an invisible cost that either reduces the amount of foreign currency you end up with or inflates the amount of Rand you have to spend.

The forex spread acts as a silent, variable tax on every cross-border transaction. Overlooking it means consistently overpaying for currency and leaving valuable capital on the table.

Finding a provider with a low or even a zero spread isn't just about saving a few cents here and there; it’s a critical financial move. It means you get cost predictability, you protect your margins, and you ultimately gain better control over your cash flow.

Forex Cost Comparison for South African Businesses

To really see the difference, it helps to compare the typical costs you'll encounter with various providers. This table quickly shows why paying close attention to the spread is a non-negotiable for any South African finance team.

| Provider Type | Typical Spread | Hidden Fees | Best Use Case |

|---|---|---|---|

| Traditional Banks | High (1-5%+) | Often include SWIFT and intermediary fees | Small, infrequent personal transactions |

| Low-Spread Brokers | Low (0.1-1.0%) | May have commissions or account fees | Active forex trading and speculation |

| Zaro (Zero Spread) | 0% | None | Business payments, supplier invoices, revenue repatriation |

As you can see, the model makes all the difference. While traditional banks are familiar, their high spreads are designed for retail convenience, not business efficiency. On the other end, specialised low-spread brokers are built for high-frequency traders, not for paying operational invoices.

A zero-spread model, like Zaro, is purpose-built to eliminate this core cost for businesses, ensuring you get the real rate every time you transact.

What the Forex Spread Really Means for Your Business

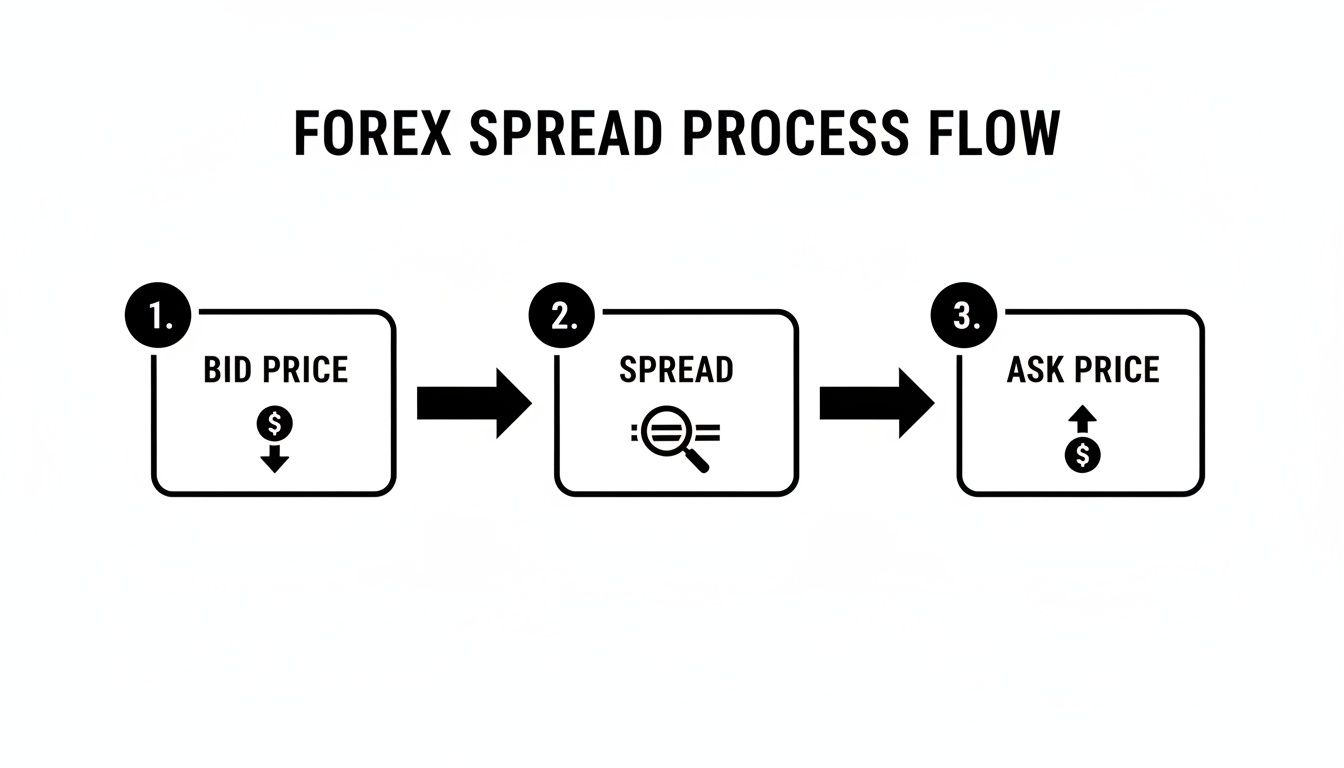

To get a real grip on why hunting for the lowest spread forex broker is so important, you first need to understand what the spread actually is. Simply put, the spread is the difference between two prices a broker gives you for any currency pair: the bid price and the ask price.

It’s just like the currency exchange booth at the airport. You’ll see a "we buy" price and a "we sell" price for US Dollars. The "we buy" price is the bid – that’s what they’ll pay you for your currency. The "we sell" price is the ask – that’s what you have to pay them. The ask price is always higher, and that gap is their profit. That’s the spread.

So, if your South African business needs to pay a supplier in dollars, you're effectively "buying" USD with your ZAR. This means you’ll always be charged the higher ask price. The spread is the broker's fee baked right into the exchange rate, and it's a direct cost to your business.

Fixed vs Variable Spreads

As you start comparing your options, you'll run into two main types of spreads. Each one has different implications for how you budget and manage your costs.

Fixed Spreads: The name says it all. This spread stays the same, no matter how wild the market gets. A broker might quote a fixed 1.5 pip spread on USD/ZAR, which means your cost is predictable every single time you make a payment.

Variable Spreads: This spread is always on the move, changing with market conditions like supply, demand, and major economic news. When things are calm, variable spreads can get incredibly tight—sometimes almost zero. But the moment volatility strikes, they can blow out, becoming much wider.

For a business that’s making operational payments, not speculating on market moves, predictability is king. A variable spread might look tempting with its promise of near-zero costs, but a sudden market swing could make paying a critical invoice far more expensive than you planned. Fixed spreads give you that certainty, but you usually pay for it with a slightly wider spread on average, as the broker takes on the risk of market volatility.

The tricky part for businesses is that neither model is really built for operational payments. You're either paying a consistently wider margin with a fixed spread or gambling on unpredictable costs with a variable one.

Understanding Your All-In Cost

Here's something many people miss: the advertised spread is only one piece of the puzzle. A provider can shout about a tiny spread from the rooftops, but they might be making up for it with hefty commissions or other hidden fees. That’s why you absolutely have to calculate your all-in cost.

This just means looking at the spread plus any commissions or other charges to see what you're truly paying. For example, one broker might offer a razor-thin 0.1 pip spread but tack on a R150 commission. Another might have a wider 0.8 pip spread but charge zero commission. You won't know which is actually cheaper for your payment size until you do the maths.

This is becoming a massive deal for South African businesses. With a trade surplus projected to hit a staggering R1.9 trillion by 2025, optimising every cross-border payment is no longer a "nice-to-have"—it's a strategic priority. The best brokers know this and are now competing aggressively on these all-in costs. We're seeing FSCA-regulated brokers offer raw accounts with spreads near 0.0 pips on major pairs, balanced by a commission per lot. For a medium-sized exporter, moving away from the high spreads charged by traditional banks can easily save hundreds of thousands of Rand every year. To see how the market is shaping up, it's worth reading some detailed regional analyses about low-spread brokers in South Africa.

How to Calculate Your True Forex Transaction Costs

Knowing what a spread is in theory is one thing. Actually calculating what it costs your business is where you can start protecting your bottom line. To properly compare different forex providers and see what you’re really paying, you need a way to work out the total cost of any transaction.

The secret is to look past the advertised rates and find your effective spread. This is your all-in cost—the spread plus any commissions—which gives you a true apples-to-apples comparison. Let’s walk through how to do the maths.

Step 1: Turn Pips into Rands

First things first, we need to convert an abstract term like "pips" into a real Rand value. The value of a pip isn't fixed; it changes based on the currency pair you're trading and the size of your transaction.

The formula is pretty straightforward:

Pip Value = (Pip Size / Exchange Rate) * Transaction Volume

For most major currency pairs, a single pip is 0.0001. Imagine your business needs to pay a $50,000 invoice to a supplier in the US, and the current USD/ZAR exchange rate is 18.5000.

Here's how you'd calculate the pip value:

- Pip Value = (0.0001 / 18.5000) * 50,000

- Pip Value = $0.27, which is about R5.00 per pip at this rate.

Suddenly, it’s clear. For every single pip in the spread, your business is paying an extra R5.00 on this one payment. You can see how a "small" spread quickly adds up to a significant cost.

This diagram shows you exactly where that cost comes from—it's the gap between the price a broker is willing to buy at (bid) and the price they're willing to sell at (ask).

That gap is the broker's built-in profit margin, and it comes directly out of your pocket.

Step 2: Calculate the Effective Spread

Now, let's factor in commissions. This is where many businesses get caught out. A broker might advertise a fantastic 0.2 pip spread but also charge a $7 commission per trade. How does that compare to a "zero commission" broker who has a 1.0 pip spread?

To figure that out, you need to convert the commission fee into pips.

Commission in Pips = Commission Fee / Pip Value

Using our example where one pip is worth $0.27:

- Commission in Pips = $7 / $0.27

- Commission in Pips = 25.9 pips

Now, just add the commission (in pips) to the broker's base spread to find your true, all-in cost.

- Effective Spread = Base Spread + Commission in Pips

- Effective Spread = 0.2 pips + 25.9 pips = 26.1 pips

And there you have it. The "low-spread" option is actually far more expensive for this transaction than the one with no commission and a 1.0 pip spread. This is why calculating your effective spread is so critical. For a quick way to model these costs, a good UK rate calculator can help you run the numbers.

Worked Example Calculating Total FX Cost on a $50,000 Invoice

Let's put this all together in a real-world scenario. A South African business needs to pay a $50,000 invoice to a US supplier. We’ll assume the real, mid-market USD/ZAR rate is 18.5000.

This table shows just how different the final cost can be depending on the provider you choose.

| Cost Component | Traditional Bank | Low-Spread Broker | Zaro (Zero Spread) |

|---|---|---|---|

| Mid-Market Rate | 18.5000 | 18.5000 | 18.5000 |

| Quoted Rate | 18.8600 (a 2% markup) | 18.5020 (a 0.2 pip spread) | 18.5000 (mid-market) |

| Spread Cost | $50,000 * (18.8600-18.5000) = R18,000 | $50,000 * (18.5020-18.5000) = R100 | R0 |

| Commission/Fees | R0 (hidden in spread) | R500 (flat fee) | R0 |

| Total Transaction Cost | R18,000 | R600 | R0 |

The numbers don't lie. The traditional bank's wide, hidden spread costs the business a staggering R18,000. The specialist broker is a massive improvement, bringing the cost down to a much more reasonable R600.

However, for operational business payments, a zero-spread model like Zaro completely eliminates this transaction friction, putting that money straight back onto your balance sheet.

Your Broker Evaluation Checklist: Looking Beyond the Spread

A broker’s headline spread is their shop window—it's designed to catch your eye and pull you in. But for any serious business, what happens inside the shop is what truly counts. The most cost-effective financial partner isn't just the one waving the lowest advertised number; it's the one that actually delivers on that promise, time and time again.

Chasing the absolute lowest spread forex broker without seeing the bigger picture can be a very expensive mistake. A tiny spread means nothing if your transaction gets delayed, filled at a worse price than you clicked on, or is handled by a shady operator. This checklist will help you cut through the marketing noise and focus on what really matters.

Regulatory Compliance: Your First and Most Important Check

Before you even glance at a fee schedule, you need to verify a provider's regulatory status. This is completely non-negotiable, especially for a business operating in South Africa.

FSCA Licensing: Is the broker regulated by the Financial Sector Conduct Authority (FSCA)? This is the single most important question you can ask. FSCA regulation means the company must follow strict local laws built to protect your money and ensure you're being treated fairly.

Global Reputation: Do they hold licenses with other top-tier regulators, like the UK’s FCA or Australia’s ASIC? A solid global regulatory footprint is a strong signal that a company takes security and transparency seriously.

Choosing an unregulated provider, no matter how tempting their spreads look, opens your business up to huge risks. You could be dealing with fraud or, in a worst-case scenario, lose all your funds with zero legal options to get them back.

Execution Speed and Slippage

This is where the advertised spread gets put to the test. Execution is all about how quickly and accurately your transaction goes through. In a fast-moving market, even a millisecond's delay can change the price you end up paying.

This brings us to a sneaky little cost called slippage. It’s the difference between the price you thought you were getting when you clicked the button and the price the transaction was actually completed at. A tiny bit of slippage is normal, but a broker with clunky technology or not enough liquidity can consistently fill your orders at a price that works against you.

Think about it this way: a broker offering a 0.1 pip spread is no bargain if you constantly get hit with 0.5 pips of negative slippage. That hidden cost just made your transaction five times more expensive, turning a great deal into a terrible one.

Always ask a potential provider about their execution speeds and what they do about slippage. A good partner will be upfront about how they handle it and will have the right tech in place to keep negative slippage to a minimum.

Account Types and Funding Options

Don't assume all accounts are the same. A broker might shout about zero-pip spreads, but often, those are reserved for special "raw" or "pro" accounts that come with high commission fees or require a massive minimum deposit.

Account Structures: Take a hard look at the different account types. Does the low-spread account actually make sense for your business’s transaction volume and the capital you have on hand? Don't let a provider shoehorn you into an account that doesn't fit.

ZAR Funding and Withdrawals: For any South African business, this is critical. Can you deposit and withdraw funds directly in South African Rand (ZAR) without getting stung by huge conversion fees? A broker that makes you convert ZAR to USD just to fund your account is adding another hidden cost and a layer of unnecessary hassle.

In the South African forex scene, this has become a key battleground for businesses needing efficient ways to handle global operations. For instance, Exness has made a name for itself among the lowest spread forex brokers by offering South African businesses spreads from 0.0 pips on major pairs. Being FSCA regulated is crucial here, especially when you consider the rand's volatility, which can easily swing 15-20% against the US dollar in a year. You can dig deeper by reading in-depth coverage of low-spread brokers in ZA.

When you're sizing up potential partners, it’s also smart to look at the broader financial services they offer. A provider that gets the full picture of business finance can often provide more complete and efficient solutions that go well beyond just forex.

Ultimately, picking the right partner is a balancing act. The lowest spread is a great place to start, but it's the combination of fair pricing, solid regulation, reliable execution, and business-friendly features that delivers real, long-term value. Use this checklist to look past the flashy numbers and make a choice that truly protects your bottom line.

A Better Way for Business Payments: The Zero Spread Model

So far, we've been diving deep into the world of forex trading, hunting for the broker with the tightest spreads. But what happens when you’re not trying to speculate on currency swings? What if you just need to pay an international supplier or get paid by an overseas client?

For day-to-day business payments, the whole conversation needs to change. It's not about timing the market; it's about efficiency, predictability, and locking down costs. You're not trying to make a profit from a ZAR/USD fluctuation—you're trying to make sure it doesn't eat into your profit. This is where the traditional broker model, built for traders, just doesn't fit the needs of a business.

When it comes to operational payments, the ultimate "lowest spread" isn't just a fraction of a pip. It's zero.

From Market Speculation to Operational Sense

A South African business has completely different priorities than a forex trader. Finance teams need a system that's secure, straightforward, and above all, crystal clear on pricing.

Think about what a business actually needs:

- Predictable Costs: You have to know exactly what a payment will cost in Rands before you hit send. A floating spread turns your budget into a guessing game.

- A Simple Process: Making a payment shouldn't require logging into a complex trading platform. It should feel as easy as a local EFT.

- Proper Admin Controls: The finance manager needs a bird's-eye view, with multi-user access and clean reports that make reconciliation a breeze.

Using a trading account for business payments is like using a Formula 1 car to do the weekly grocery run. Sure, it’s powerful, but it's completely impractical and built for a totally different purpose.

How Does a Zero Spread Model Actually Work?

This is where modern payment platforms designed for businesses come in. They operate on a fundamentally different principle. Instead of acting as a middleman and tacking on a markup, they give you direct access to the real, mid-market exchange rate—the same rate banks and massive financial institutions use to trade amongst themselves.

It's a simple but powerful idea: by getting rid of the spread, the platform removes the single biggest hidden cost in sending money abroad. Your business gets the true, untouched exchange rate. No markups, no nasty surprises.

This completely changes the game for small and medium-sized businesses operating internationally. Instead of seeing a percentage of your revenue skimmed off every single transaction, that capital stays right where it belongs: in your business, improving cash flow and boosting your bottom line. Forex stops being a frustrating cost centre and becomes just another transparent part of your operations.

What This Means for South African Businesses

This shift is a massive deal for South African companies. Our local forex market is incredibly active, thanks in part to a booming export sector valued at R1.8 trillion. This has pushed FSCA-regulated brokers to offer incredibly tight spreads for traders—think average spreads of just 0.1 pips on EUR/USD. While that's great for speculators, as we've learned more from resources like the FXScouts guide to low-spread brokers in SA, even that tiny spread (plus commission) is a needless expense for a business that just needs to settle an invoice.

When you switch to a zero-spread model built specifically for B2B payments, the advantages are immediate and obvious:

- Real Cost Savings: By cutting out both the spread and sneaky SWIFT fees, more of your money stays yours.

- Smarter Cash Flow: When costs are predictable and transparent, you can budget with far more confidence.

- Less Admin Headache: A simple, direct payment system frees up your finance team's time for more important work than reconciling confusing forex fees.

For any business, the search for the "lowest spread forex broker" should end with a simple realisation: the best spread is no spread at all. It’s this model that delivers the clarity and efficiency you need to compete on the global stage.

Common Questions About Forex Spreads

When you're dealing with international payments, a lot of questions pop up. It's totally normal. Here are some straightforward answers to the things South African business owners ask us most, helping you cut through the noise and make the right call for your company.

What’s Considered a “Good” Forex Spread for My Business?

In the fast-paced world of online trading, a raw spread of 0.0 pips on major currency pairs is the holy grail. But let's be clear: trading and business payments are two very different things. For your business, any spread is a cost you shouldn't have to pay.

Sure, finding a provider offering a 0.5 pip spread is miles better than the 50 pips your bank might be charging. But the real win for paying invoices or suppliers is a true zero-spread model. This approach uses the real mid-market rate, which means the spread cost is completely removed, giving your business total transparency and maximum savings.

Why Does FSCA Regulation Matter So Much?

The Financial Sector Conduct Authority (FSCA) is the watchdog for financial services in South Africa. Partnering with an FSCA-regulated provider isn't just a box to tick; it’s a non-negotiable for protecting your business.

Here’s why it's so critical:

- Your Money is Protected: It ensures your funds are safeguarded under South African law.

- They Play by the Rules: The provider is held to strict standards of transparency and fair dealing.

- You Have Backup: If a dispute arises, you have a local, official body to turn to for help.

Going with an unregulated provider—even if they promise the "lowest spread"—is a huge gamble. You're exposing your business to serious risks like fraud or even losing your money entirely, with no local legal authority to help you get it back.

Choosing an FSCA-regulated partner isn't just a good idea—it's a fundamental requirement for securing your business's financial operations. Overlooking this puts your company's capital directly at risk.

Can I Just Use a Trading Broker to Pay My International Suppliers?

You could, but it’s a really bad idea for your business operations. Trading platforms are built for speculation—making bets on currency movements. They are not designed for the practical reality of paying B2B invoices.

If you try to use one, you'll likely run into frustrating funding processes, long payment delays, and potential compliance headaches. A dedicated business payment platform, on the other hand, is built from the ground up for exactly these kinds of transactions. It gives you smoother onboarding, better controls for your finance team, and a much more secure and efficient way to manage payments.

What's the Catch with "Zero Commission" Forex Brokers?

Be wary when you see "zero commission." It's more of a marketing slogan than a reflection of the true cost. Providers who shout about having no commission almost always make their money by hiding their fee in a wider, less favourable spread.

You won't find a line item for "commission" on your statement, but make no mistake, you are paying for their service through the poor exchange rate you receive. This is exactly why you need to calculate your "all-in cost" by comparing their rate to the live mid-market rate. A provider who is upfront about a small commission but gives you a near-zero spread is almost always offering a more honest and better-value deal.

Ready to eliminate spreads and hidden fees from your international business payments for good? Zaro offers South African businesses direct access to real exchange rates with zero markup. See how much you can save on your next international transaction. Discover true cost-effective payments with Zaro.