If you've ever typed "what is equity forex" into a search bar, you're in good company. It's a confusing term mainly because it isn't one specific financial product. Instead, it describes two very different ideas that impact businesses and traders in completely different ways. For any South African company, figuring out which one matters to you is the first step in protecting your bottom line from currency swings.

Decoding 'Equity Forex' for South African Businesses

The confusion around "equity forex" stems from its two distinct meanings. One lives in the fast-paced world of speculative forex trading. The other is a critical concept for the financial health of any South African business that buys or sells internationally. Let's untangle them.

For a forex trader, equity is simply the live value of their trading account. It's the cash they have on hand plus or minus the paper profit or loss from any open trades. This number bounces around every second the market is open and is a vital yardstick for managing their risk.

But for a business owner, exporter, or CFO here in South Africa, the idea is much more fundamental. In your world, "equity forex" is all about how currency movements impact your company's balance sheet equity—in other words, the net worth of your entire business.

Two Sides of the Same Coin

Imagine your company's value is a ship charting a course toward its long-term financial goals. The unpredictable ocean currents and weather? That's currency volatility. A favourable exchange rate acts like a strong tailwind, pushing you forward by boosting profits and growing your company's value. An adverse shift, however, is a headwind that can erode revenue and shrink your equity.

For an export business, managing the "forex" aspect of your operations is really about protecting the "equity" you've worked so hard to build. It’s about making sure a sudden storm in the currency markets doesn’t capsize your ship.

This second meaning is where the real risk—and opportunity—lies for South African businesses. An exporter who prices their goods in US dollars, for instance, faces a direct threat to their ZAR-based equity if the Rand suddenly strengthens. That dollar revenue, once converted, buys fewer Rands, which directly squeezes profit margins and shrinks the company's retained earnings.

To make this crystal clear, it helps to see who is most concerned with each definition.

Two Meanings of Equity in a Forex Context

This table offers a quick summary of the two main interpretations of 'equity forex' and who they typically apply to.

| Concept | What It Means | Who It Affects Most |

|---|---|---|

| Trading Account Equity | The real-time value of a speculative forex trading account, including unrealised profits or losses. | Individual and institutional forex traders. |

| Balance Sheet Equity | The company's net worth, which is impacted by the realised value of foreign currency transactions. | Exporters, importers, CFOs, and business owners. |

Knowing which definition of "equity forex" applies to your situation is crucial. A trader is focused on managing the short-term value of their account. A business leader, on the other hand, has a much bigger job: safeguarding the long-term financial foundation of their entire company.

How Forex Volatility Impacts Your Balance Sheet Equity

For South African exporters, the term "equity forex" isn't some abstract trader's jargon—it's a real-world force that plays out directly on the balance sheet. This is where currency movements can either build up your company's value or chip away at it. To really get a handle on this, we need to talk about foreign exchange (FX) exposure.

Imagine a Stellenbosch wine exporter who has just sealed a great deal, selling their premium Pinotage to a distributor in the United States. They agree on a price of $100,000, and the invoice is issued in US dollars. On the day the deal is signed, the exchange rate is a comfortable R18.50 to the dollar. On paper, that sale is worth a cool R1,850,000.

The catch? The payment term is 60 days. And in the world of currency, 60 days is a lifetime.

The Rand Strengthens: A Hidden Threat

Fast forward two months. The US distributor pays the invoice on time, but the Rand has strengthened against the dollar. The new exchange rate is R17.90. That same $100,000 payment, once converted back home, is now worth only R1,790,000.

Just like that, the company has lost R60,000 of expected revenue. This isn't just a small accounting adjustment; it’s a direct blow to the company's bottom line and, ultimately, its equity. The cost to produce that wine didn't change, but the value received for it did, all because the forex market shifted.

The real challenge of managing equity forex is protecting your company's net worth from these unpredictable market swings. A few percentage points of currency fluctuation can be the difference between a profitable quarter and an unexpected loss.

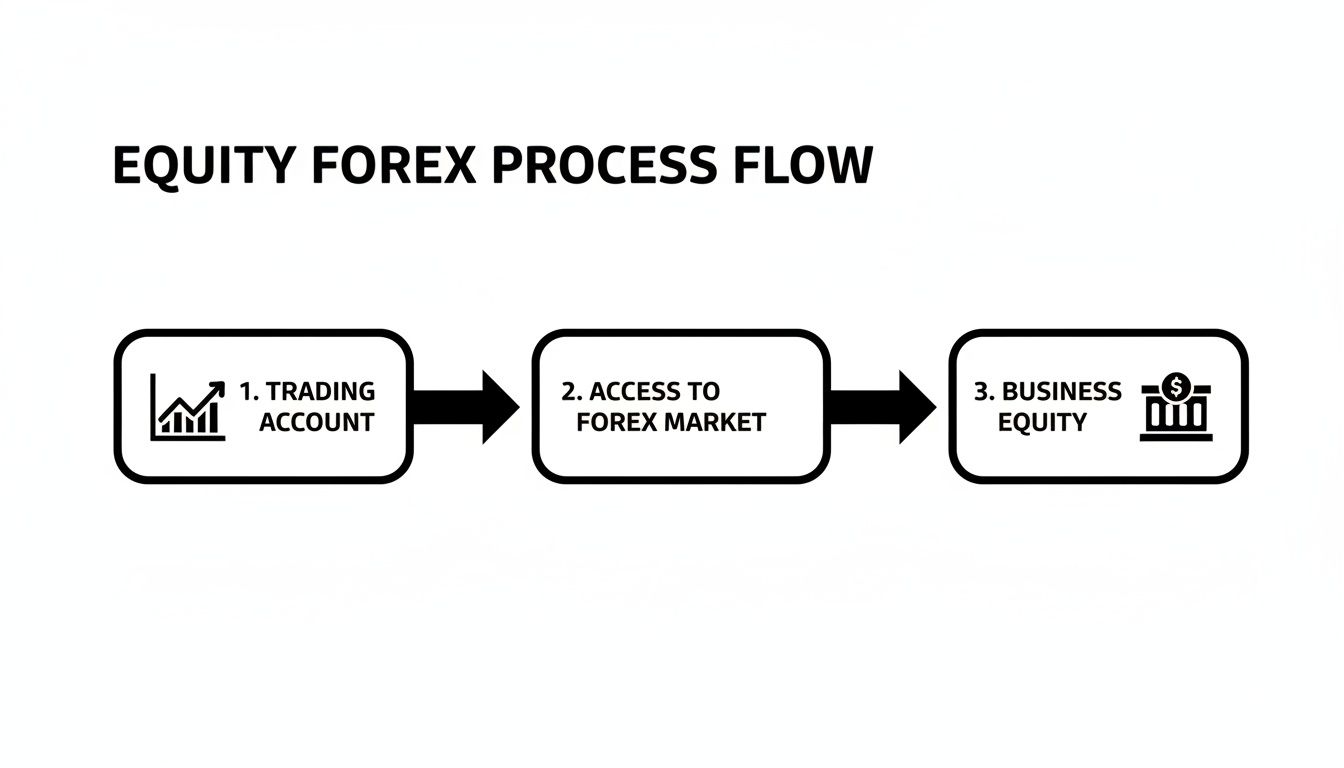

This process flow shows exactly how a forex transaction trickles down to impact your business's equity.

As the diagram illustrates, what begins as a simple currency exchange has a very real effect on the overall financial health and value of the business.

This isn't a rare occurrence; it’s a daily reality for businesses all over South Africa. And as our trade grows, so does the risk. South Africa's foreign exchange market hit USD 3,861.60 million in 2024 and is forecast to reach USD 6,852.50 million by 2033. This growth is driven by strong international trade and the shift to digital trading platforms—which, thankfully, also means better tools are available for businesses to manage their cross-border payments.

From Revenue Fluctuation to Equity Erosion

So, how does a R60,000 shortfall on a single invoice actually erode a company’s equity? The link is direct, and it runs straight through your financial statements.

- Lower Retained Earnings: Profit is what fuels your retained earnings, a core part of shareholder equity. When forex losses eat into your net income, less cash is added to those earnings, slowing down your company's value growth.

- Compressed Profit Margins: If you're constantly taking hits from negative currency movements, your profit margins get squeezed. This makes the business less appealing to investors and can make it harder to get financing for growth.

- Inaccurate Financial Forecasting: Volatility makes budgeting and forecasting a nightmare. A business plan built on an R18.50 exchange rate can fall apart if the rate spends most of the year closer to R17.90.

This is the cumulative effect we’re talking about. Every cent lost to a bad exchange rate is a cent that could have been reinvested, paid out to shareholders, or used to build a stronger financial foundation. To get a better grip on how all these pieces fit together, a good starting point is understanding key financial ratios from your financial statements.

Ultimately, this makes proactive currency management more than just a treasury function—it's a strategic necessity for protecting the hard-earned value of your business.

The Hidden Transaction Costs Eroding Your Business Value

Beyond the wild swings of the forex market, there’s a quieter, more predictable threat chipping away at your business value with every single transaction. These are the hidden costs baked into traditional cross-border payments—the small percentages and vague fees that act like a slow, steady leak in your financial pipeline, draining your equity.

While you can’t control currency volatility, these transaction costs are a different beast entirely. They’re frictional, unnecessary losses that happen in the simple act of moving money. Every rand lost here is a rand that should have been part of your retained earnings, the very foundation of your company's equity.

The Anatomy of Hidden Fees

When you get paid from overseas through the usual banking channels, the amount that lands in your account is almost never what your client actually sent. Why? Because several fees, some obvious and some cleverly disguised, get skimmed off along the way.

These costs are often buried in convoluted statements or simply absorbed into a poor exchange rate, which makes them incredibly difficult to spot. But make no mistake, their cumulative effect on your company's bottom line can be staggering.

Here are the main culprits silently eating into your revenue:

- The Exchange Rate Spread: This is the big one, the most significant hidden cost by far. Banks show you a "client rate," which is a marked-up version of the real mid-market or "spot" rate. That difference, the spread, is pure profit for them and can easily cost you 1-4% of your transaction's value.

- SWIFT Fees: The SWIFT network is the messaging system banks use to talk to each other for international transfers. The sending bank, your receiving bank, and any intermediary banks that touch the money can all charge a fee for their part in the process.

- Receiving Charges: On top of everything else, many local banks will charge you a flat fee just for the "service" of processing and depositing an incoming international payment.

Think of it like this: The exchange rate spread is a percentage tax on your revenue that you never agreed to pay. It’s a direct transfer of your company's value to the bank, hidden in plain sight.

A Practical Example: The R1,000,000 Payment

Let's bring this home with a real-world scenario for a South African business. Imagine you're due a payment of $55,555 from a client in the US. At the real exchange rate of R18.00 to the dollar, that invoice is worth exactly R1,000,000. Simple enough.

But your bank doesn't give you that real rate. Instead, they offer you a rate of R17.55, having built in a hefty 2.5% spread for themselves.

Here's the damage:

- Payment Value at Real Rate: $55,555 x 18.00 = R1,000,000

- Payment Value at Bank Rate: $55,555 x 17.55 = R975,000

Just like that, R25,000 of your hard-earned revenue has vanished into thin air. And that’s before accounting for the extra SWIFT and receiving fees, which could easily shave off another R500 to R1,000.

This R25,000+ shortfall isn't just another "cost of doing business." It is a direct hit to your net profit. It's money that should have boosted your retained earnings, strengthened your balance sheet, and ultimately, increased your company's equity.

When this happens on every single international transaction, the annual loss becomes a serious drain. These preventable leaks weaken your company’s financial foundation, making you more vulnerable to the very market risks you’re trying to manage. Plugging them isn't just about saving on fees—it's a critical strategic move to protect and grow the business equity you’ve worked so hard to build.

Practical Strategies to Protect Your Equity from Forex Risk

Knowing how forex risk and hidden fees can eat into your company’s equity is one thing. Actually doing something about it is another. For South African CFOs and business owners, protecting your bottom line doesn’t have to involve bewildering financial instruments. It’s about being smart and practical to build a wall of certainty in a market that loves uncertainty.There are several proven ways to shield your business from currency whiplash. These methods can turn forex management from a reactive headache into a proactive, strategic advantage. Each one has its own pros and cons, so the trick is picking the right tool for your specific business model and how much risk you're comfortable with.

To properly safeguard your equity, it's crucial to weave proven risk management best practices into the fabric of your business. This goes beyond just forex hedging and builds a more resilient company overall.

Employing Natural Hedging

One of the most elegant and straightforward strategies is what we call natural hedging. At its core, this is about creating an organic balance between the foreign currency you earn and the foreign currency you spend. You’re essentially building an internal buffer against market swings without touching a single formal financial product.

Picture this: your company earns US dollars from its exports. Instead of immediately converting that money to Rands, you use those same dollars to pay for imported raw materials, international software subscriptions, or even your overseas marketing agency—all of which are priced in USD. By keeping the funds in the same currency, you skip the conversion process entirely. You completely sidestep the risk of the exchange rate moving against you.

This approach is a game-changer for businesses that have a healthy flow of both income and expenses in the same foreign currency. Its biggest advantage? It’s incredibly cost-effective, saving you the fees that come with formal hedging tools.

Locking in Rates with Forward Contracts

For a more structured approach, you can turn to a forward contract. This is a simple agreement with a financial provider to swap a set amount of currency on a future date, but at a rate you agree on today. It’s like putting a pin in the exchange rate, giving you absolute certainty for a future transaction.

Let's go back to our Stellenbosch wine exporter who is waiting on a $100,000 payment in 90 days. They're worried the Rand might strengthen, which would mean fewer Rands in their pocket. They can sign a forward contract to sell those dollars at today's rate—let's say it's R18.50.

This simple move creates powerful certainty:

- Budgeting Confidence: They know they will receive precisely R1,850,000, regardless of what the live exchange rate is doing in three months' time.

- Margin Protection: Their profit margin is now safe and won't be wiped out by a sudden currency shift.

- Simplified Planning: Financial forecasting becomes far more reliable, which allows them to make better strategic decisions for the business.

The only real downside is that you miss out on potential upside. If the Rand weakens to R19.50, they’re still locked into their R18.50 rate. For most businesses, however, the peace of mind that comes with absolute certainty is far more valuable than a speculative long shot.

The global forex market has seen immense growth, with trading volumes surging by 28% between 2022 and 2025, from USD 7.5 trillion to USD 9.6 trillion. This expansion, driven largely by volatile central bank policies, highlights the critical need for South African businesses to manage currency risk effectively. With spot transactions making up nearly a third of this activity, platforms like Zaro, which offer real spot rates, provide a vital advantage in this dynamic environment. Discover more key forex trading statistics and their implications for business.

Gaining Flexibility with Currency Options

What if you want protection but don't want to miss out on favourable market moves? That's where a currency option comes in. An option gives you the right, but not the obligation, to buy or sell a currency at a set price on or before a certain date. For this flexibility, you pay a fee, known as a premium.

Think of it like an insurance policy for your exchange rate. If the rate moves against you, you can exercise your option and lock in your protected rate. But if the rate moves in your favour, you can just let the option expire and trade at the much better live market rate. You get the best of both worlds.

Shifting Risk with Strategic Invoicing

Finally, we have the most direct strategy of all: strategic invoicing. This simply means you bill your international clients in South African Rands (ZAR). By doing this, you neatly pass the entire currency conversion risk onto your customer. You know exactly how much ZAR will land in your account, giving you 100% financial certainty on that sale.

While it’s the safest route for you, it can sometimes make your business less competitive. Many international buyers prefer the simplicity of being invoiced in a major currency like USD or EUR. Whether this works often comes down to the norms in your industry and the strength of your client relationships.

How Transparent FX Solutions Can Bolster Your Equity

We’ve walked through the traditional ways of managing forex risk, and it’s become clear that while they might tackle market swings, they do nothing about the costly friction baked into the payment process itself. A modern approach needs to do both. It's about protecting your business from volatility and stopping the slow, preventable bleed caused by inefficient, opaque banking systems.

The fundamental issue with old-school banking is the complete lack of transparency. Hidden spreads and a maze of vague fees are a direct assault on your bottom line and, by extension, your company’s net worth. A truly transparent FX solution, like the one we’ve built at Zaro, is designed to eliminate these value-destroying costs from the ground up. It gives you direct access to the real mid-market exchange rates—the ones you see on the news—with a simple, upfront fee.

Recalculating the Wine Exporter's Profit

Let's go back to our Stellenbosch wine exporter and their $100,000 invoice. Earlier, we saw how a strengthening Rand could wipe out their profit. But what happens even if the market doesn't move?

Let's say the rate holds steady at a favourable R18.50. If they use a traditional bank that charges a 2.5% spread, their expected R1,850,000 revenue suddenly shrinks to just R1,803,750. That’s a loss of R46,250 before a single SWIFT or admin fee is even considered.

This isn't a market risk; it's a processing cost. That R46,250 is pure profit that was siphoned away from the business—money that should have gone straight into retained earnings to build the company’s equity.

With a transparent FX partner, you treat currency conversion like any other business service: you pay a fair, visible fee for a clear result. You stop paying an invisible tax that punishes your success.

Using a platform that offers the real exchange rate with a clear, low fee changes the entire picture. Almost all of that R46,250 flows directly back to the company’s bottom line. This isn't just a one-off saving. It’s a permanent boost to your profitability on every single international transaction, compounding over time to significantly strengthen your balance sheet.

A Clearer Financial Picture

To make this crystal clear, let's put the numbers side-by-side. The table below illustrates the real financial impact of using a transparent provider like Zaro versus a traditional bank for that same $100,000 transaction.

Traditional Banks vs Zaro: A Cost Comparison

| Fee Component | Traditional Bank (Estimate) | Zaro |

|---|---|---|

| Exchange Rate | Marked-up rate (e.g., R18.03) | Real Spot Rate (e.g., R18.50) |

| Hidden Spread Cost | R46,250 | R0 |

| Transaction Fee | Buried in the rate | Small, transparent percentage |

| SWIFT & Receiving Fees | R500 - R1,500 | R0 |

| Total Value Kept | ~R1,802,250 | ~R1,840,000+ |

Note: Table is for illustrative purposes on a $100,000 transaction.

The difference is stark. The cost isn't just a number on a spreadsheet; it's real value that either stays in your business to fuel growth or gets quietly skimmed off the top by your bank.

Beyond Savings: Operational Efficiency That Protects Equity

Protecting your company’s value isn't just about cutting costs; it's also about reducing operational risk and administrative drag. The clunky, outdated systems used by many banks are slow and create mountains of unnecessary work for your finance team—another hidden cost that eats away at your resources.

A modern financial platform strengthens your equity from every angle by improving your day-to-day operations:

- Faster Onboarding: Have you ever waited weeks for a bank to complete its Know Your Business (KYB) checks? That’s weeks you can’t transact. A streamlined digital process gets you fully set up and ready to trade in a matter of days.

- Integrated Accounts: Having ZAR and USD accounts under one roof drastically simplifies treasury management. You can hold foreign currency, pay international suppliers in their preferred currency, and convert funds only when the timing and rate are right for you.

- Better Team Controls: Enterprise-grade features like multi-user access and custom permissions give your finance team the control they need to manage payments securely, dramatically reducing the risk of human error or fraud.

Each of these efficiencies frees up your team’s time, slashes the chance of costly mistakes, and gives you far greater control over your cash flow. By removing the financial friction and operational headaches, you’re not just saving money; you're building a more resilient, valuable, and equitable business.

Here's the rewritten section, crafted to sound human-written, natural, and expert for a South African audience.

Getting South African Forex Regulations Right

If your business moves money across South Africa’s borders, you know that compliance isn't just a box-ticking exercise. It's fundamental. The rules from the South African Reserve Bank (SARB) are there for a reason—to keep the national economy stable—but for a busy finance team, they can feel like a maze.

Getting comfortable with these regulations is the only way to operate with real confidence. A big piece of this puzzle is Balance of Payments (BOP) reporting. Put simply, this means you have to declare the why behind every single international transaction. It's how the SARB keeps tabs on the money flowing in and out of the country.

Get this wrong, and you're looking at more than just a slap on the wrist. We're talking hefty fines, frustrating payment delays, and a knock to your reputation—all of which can chip away at your company's hard-earned equity.

Juggling Compliance in a Volatile Market

The South African market has its own unique flavour of challenges. The Rand is a major emerging market currency, which means it brings both big opportunities and wild swings, often at the mercy of global interest rate decisions and commodity prices.

You can see this tension in the country's external position. South Africa's forex reserves recently climbed to a record USD 72.07 billion in late 2025. While that’s a great sign of national financial health, the day-to-day currency movements make it incredibly tough for businesses to forecast accurately. You can dig deeper into South Africa's forex reserve trends and their market implications for more context.

To thrive here, you have to wear two hats: one for managing market risk and another for staying perfectly aligned with the rules. A slip-up in one area will almost always hurt you in the other, putting your business value on the line.

How a "Compliant-by-Design" Platform Changes the Game

This is where having the right financial platform stops being a nice-to-have and becomes a strategic tool. Instead of treating compliance as a manual chore bolted on at the end, a "compliant-by-design" system builds it right into your payment process from the start.

Here’s what that looks like in practice:

- Reporting on Autopilot: The system automatically sorts your transactions and preps the BOP reports, saving your team from hours of tedious admin.

- Cutting Out Human Error: When the process is standardised and automated, the chances of a simple mistake triggering a major compliance headache drop dramatically.

- A Crystal-Clear Audit Trail: Every payment is logged and reported correctly. This gives you a clean, transparent record for your own governance and for the SARB if they ever come knocking.

Partnering with a provider that genuinely gets the local regulatory environment turns compliance from a constant worry into a smooth, background process. This isn't just about avoiding penalties. It’s about freeing up your team’s time and energy to focus on what really matters: growing the business and building its equity.

Answering Your Questions About Forex and Business Equity

When you're dealing with foreign exchange, a lot of questions pop up, especially when it comes to protecting the value you've worked so hard to build in your business. Let's tackle some of the most common queries we hear from South African business owners and CFOs about managing forex and keeping their equity safe.

How Often Should We Review Our Forex Exposure?

For any business that regularly deals with international payments, a quarterly review is a great starting point. It creates a steady rhythm for checking your risks and tweaking your strategy without getting bogged down by the daily chatter of the market.

But when the Rand gets particularly volatile, waiting three months can feel like an eternity. During those turbulent times, it’s much smarter to check in monthly, or even weekly. This keeps you on the front foot, ready to react to sudden currency shocks, protect your cash flow, and stop unexpected swings from taking a bite out of your equity. Modern finance platforms can even help you keep an eye on this almost in real-time.

Think of a regular forex exposure review as a routine health check for your company's financial resilience. It helps you spot potential trouble long before it can do serious damage to your bottom line.

Are Formal Hedging Strategies Really for Small Businesses?

They absolutely can be. While you probably don't need complex derivative structures, simple and effective tools like forward contracts are surprisingly accessible. They offer incredible certainty for your budgeting and financial planning because you get to lock in a future exchange rate today.

The trick is to balance the cost of the hedge against the potential pain of doing nothing. For smaller, more frequent international payments, a more practical approach might be to use a fintech platform that gives you real-time, low-cost conversions. This can often be more efficient than setting up formal hedges for every single transaction.

What’s the Difference Between the Spot Rate and the Rate My Bank Gives Me?

This is one of the most important things to understand, as it directly hits your company's value. The spot rate is the live, mid-market price for a currency pair at any given moment—it's the genuine rate you'll see on financial news sites.

The rate your bank offers you, on the other hand, is almost always the spot rate plus their "spread" or "markup." This is just a hidden profit margin they bake in for themselves. This spread can easily shave 1-4% off your transaction's total value, which is a direct hit to your profits and, over time, your business equity. Platforms built on transparency cut out this costly hidden fee by giving you direct access to the real spot rate.

Should I Invoice International Clients in ZAR or Their Currency?

Invoicing in ZAR gives you total certainty. You know precisely how much will land in your account, which makes financial planning a whole lot easier. You’ve effectively shifted all the currency risk onto your client.

The downside? It might make you less competitive. Many international buyers prefer the simplicity and predictability of being billed in a major currency like USD or EUR. If you decide to invoice in a foreign currency, it's absolutely critical to have an efficient, low-cost conversion partner to protect your margins when you repatriate that money.

Stop letting hidden fees and unpredictable exchange rates chip away at your business equity. With Zaro, you get access to real exchange rates with zero spread, completely transparent fees, and a platform built to make your international payments simpler. See how much you could save and strengthen your bottom line by visiting https://www.usezaro.com.